How cheap Chinese exports made us all better off

5 min

China Shock 1.0—the ‘first China shock’ (2000–2007)—stemmed from China’s structural overproduction. A flood of low-cost imports boosted global purchasing power but eliminated nearly a million US manufacturing jobs. Yet for Western economies, the net effect remained positive. Will China Shock 2.0 follow the same pattern?

A current account that speaks volumes

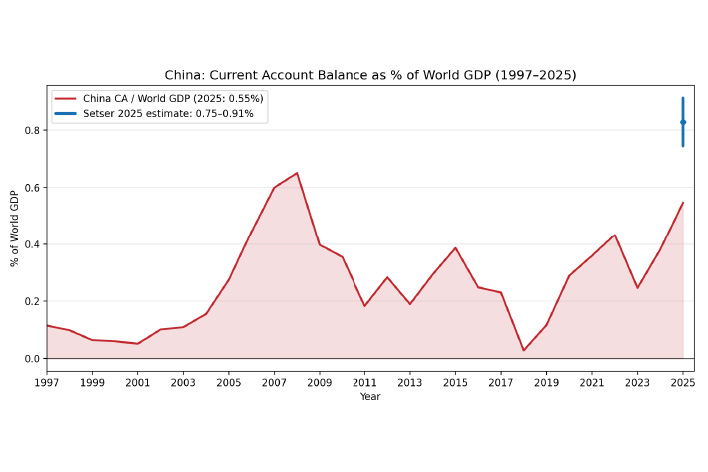

One chart tells the story of China’s export model since the 2000s: its current account balance as a percentage of global GDP. From near-zero in the early 2000s, it surged to a 0.65% surplus by 2007. At the peak of the first shock, the world was awash with cheap electronics and dubious quality ‘Made in China’ goods. Then came the Global Financial Crisis: Western spending plunged, and by 2018, China’s surplus had fallen back near zero.

Record highs

Since then, the surplus has climbed again, approaching its previous peak. Brad Sester, a trade expert at the Council on Foreign Relations, argues that IMF figures understate China’s true current account surplus. Today, it may have hit a new record - somewhere between 0.75% and 0.91%.

Record or not, the trend is clear: after the first China shock, a second wave is building. Should we welcome it or be concerned? Today, we examine the causes and consequences of the first shock. Next time, we’ll explore what’s happening now.

Production outstrips consumption

The mechanism behind China Shock 1.0 was simple: China produced far more than it consumed, exporting the excess. Factories in Shenzhen ran around the clock; container ships plied global routes. Ports in Antwerp, Rotterdam, and Long Beach unloaded vast quantities of affordable goods.

Chinese firms prospered but Chinese consumers saw little benefit. A surplus of this scale meant domestic consumption was suppressed. As a share of GDP, household spending fell from 46% in the late 1990s to 35% by 2008 (compared to 55–60% in comparable Asian economies). For the rest of the world, it initially felt like an endless windfall.

Cheaper goods for low-income households

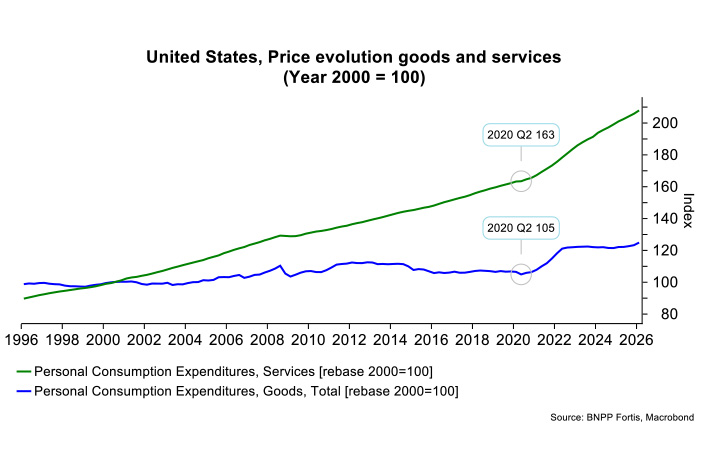

In the US, physical goods prices rose by just 5% between 2000 and the start of the COVID-19 pandemic. Everyday items like washing machines, cars, and even clothing became cheaper and more accessible, largely due to Chinese imports. A study by Jaravel and Sageri quantified this effect: every 1% increase in Chinese imports lowered goods prices by roughly 2%. Crucially, this benefit primarily helped low-income households, which spend a larger share of their budget on goods.

These affordable products also offset the 60% rise in service prices, which were harder to trade before digital services emerged. In the eurozone, the gap between goods inflation (30%) and services inflation (46%) was narrower but still significant.

1 million lost manufacturing jobs

Yet these low-cost goods came at a price, and someone had to pay it. Around 1 million US manufacturing jobs vanished, concentrated in single-industry towns: furniture factories in North Carolina, textile mills in Tennessee, and dozens of ‘company towns’ that suddenly lost their purpose. The 2013 study by Autor, Dorn, and Hanson quantified this impact, turning ‘China Shock’ into an economic, and later political, buzzword. In a 2016 update, they revised the figure to 1 million lost manufacturing jobs and 2.4 million total, accounting for indirect effects on supply chains and regional spending between 1999 and 2011.

Europe’s bill was less steep - not because its firms were smarter, but due to stronger social safety nets and worker protections that softened the blow. Other studies confirm this: Europe’s version of the China Shock was real but far less devastating than America’s.

Net positive, but not painless

The headline numbers, however, need context. Each lost job generated roughly $400,000 in consumer surplus - about 6 times the average US annual salary. Spread across 84 million households, this translated to $1,500 in extra purchasing power per year. Cumulatively, the overall balance sheet was positive.

But - and this is often lost in political debates - a net positive doesn’t mean everyone won. The benefits were spread thinly among millions of consumers, each saving a little. The costs, however, were concentrated in communities with no economic alternatives, where a factory closure didn’t just mean ‘1 fewer job’ but the collapse of an entire town. Low-income households gained the most from cheaper goods but also bore the brunt of job losses. While the macro-level outcome was positive, the human cost was far from painless.

The verdict

4 major academic studies (by Caliendo, Dix-Carneiro, Rodríguez-Clare, and Kim) independently reached the same conclusion: even the US benefited overall from China Shock 1.0, despite the loss of a million jobs. The doomsday predictions of the time proved overblown.

The pressing question now is: Will China Shock 2.0 follow the same script? We’ll explore that next week.