Pocket money: how much and from what age?

5 min

While most parents start giving pocket money to their children from the age of 12, a significant number begin earlier, during primary school (ages 6–9). The recommended amount generally ranges from €0.50 to €1 per year of age per week (i.e. between €24 and €48 per month for a 12-year-old).

A survey conducted by Maison Slash among 500 Belgian parents reveals their habits regarding when to start giving pocket money, how much to give, and how to do so. Liesje Vanneste, a financial education expert, comments on the results and shares her advice on helping young people become financially independent.

Key findings:

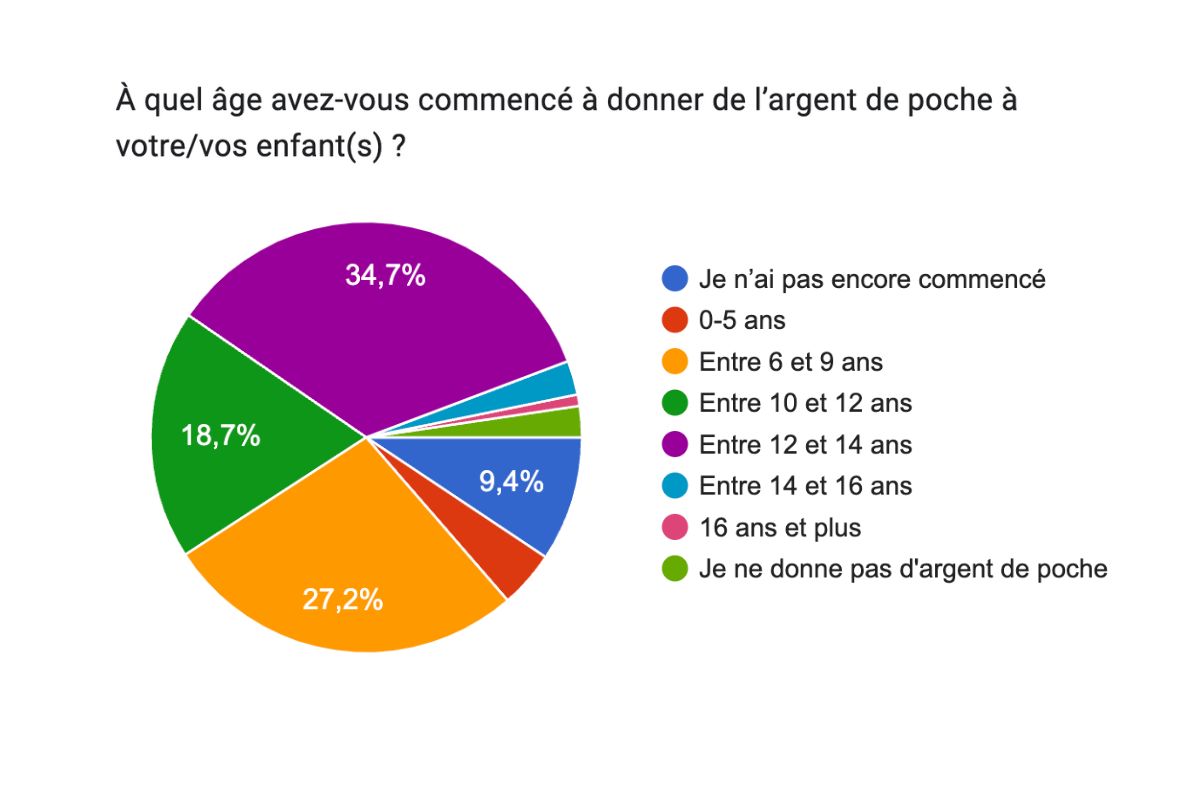

- 34.7% of parents start giving pocket money at the age of 12, while 27.2% begin between the ages of 6 and 9.

- Most parents give pocket money electronically.

- Half of parents give pocket money monthly, while 37.4% do so weekly.

- Only 2.3% of surveyed parents do not give pocket money.

- The recommended amount is between €0.50 and €1 per year of age per week.

Source: BNP Paribas Fortis survey in collaboration with Maison Slash (2025).

Understanding pocket money and its educational role

The survey shows that many parents start giving pocket money at the age of 12 (34.7%). This is understandable, given that teenagers often have more freedom and needs than younger children. However, 27.2% of parents start giving pocket money between the ages of 6 and 9.

Pocket money is a modest sum regularly given by parents to cover a child’s non-essential personal expenses. It is more than just a financial transfer; it is also a learning tool that helps young people to develop independence and understand the value of money before they enter adulthood.

The benefits of pocket money

Pocket money helps children to learn the basics of budgeting on a small scale. With a limited amount, they discover how to prioritise different wants and needs. This experience helps them to develop the ability to make thoughtful financial decisions.

Another major benefit is learning to save. When they want something that exceeds their immediate budget, they naturally realise the need to plan and save. This understanding of saving will benefit them throughout their lives.

Why starting early matters

According to Liesje Vanneste, it is useful to start giving pocket money from primary school age. By this age, children have developed basic numeracy skills and are less susceptible to external influences and peer pressure.

The earlier financial education begins, the more effective it is. Good financial habits are easier to establish before adolescence, when social influences and spending temptations increase.

The ideal age to start giving pocket money

Main age groups

Between the ages of 6 and 9, children develop their first calculation skills at school. This is a good time to introduce them to basic financial concepts, as they are not yet under much social pressure. Children can learn without facing the complexity of the external influences that teenagers do.

Starting secondary school at around age 12 often marks a turning point. Their needs evolve to include going out with friends, making personal purchases and taking part in various activities. For many families, this stage justifies increasing or starting pocket money.

Factors to consider include the child’s maturity and numeracy skills, as well as their actual social needs. Every child develops at their own pace.

According to the survey, only a small proportion of parents (2.3%) do not give pocket money.

Infographic only available in French

“You are of course not obliged to give your child pocket money. It is only possible if your finances allow it. Pocket money is a good learning tool, but there are different ways to teach financial skills. You can involve your children in certain financial decisions, for example by discussing how you save as a parent and how you manage the household budget.”

Liesje Vanneste, financial education expert

Recommended amounts and payment methods

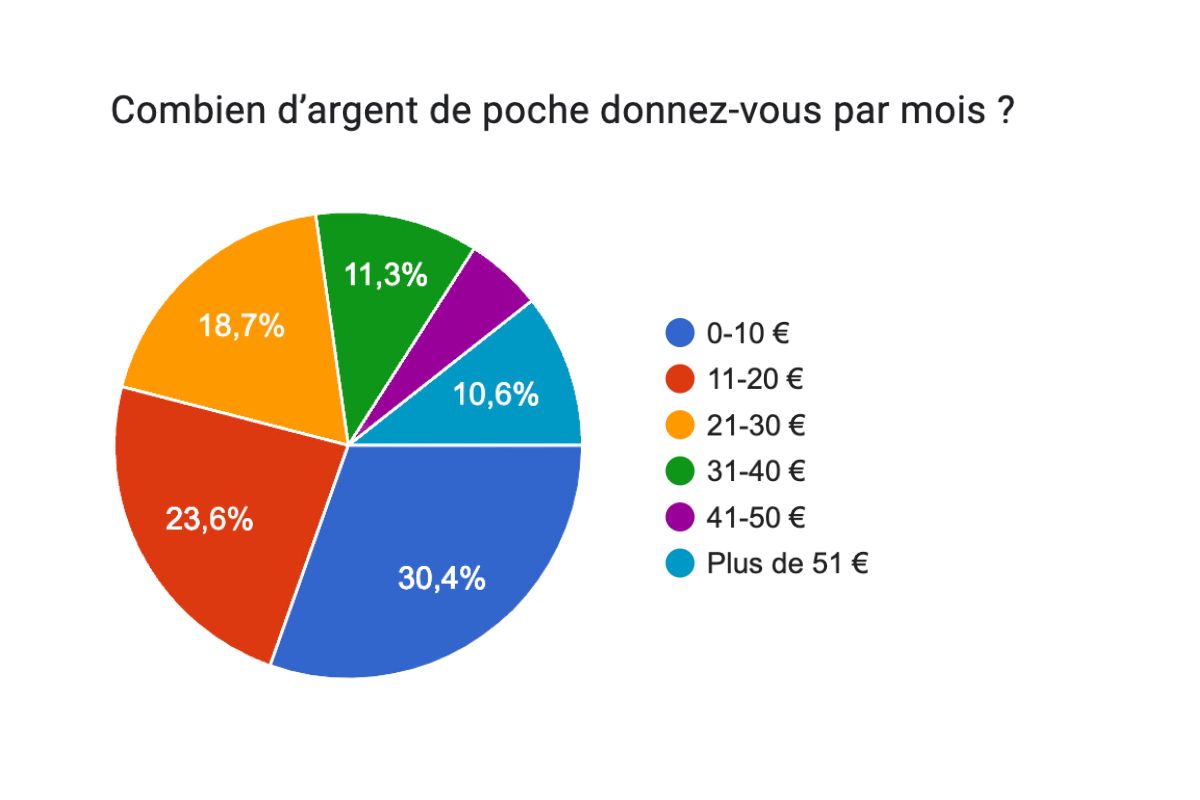

As for the amount, Liesje recommends the following guideline: €0.50 to €1 per year of age per week. This generally matches children’s needs at each age.

Table of amounts by age

| Age | Pocket money per week | Pocket money per month |

| 6 years | €3 - 6 | €12 - 24 |

| 10 years | €5 – 10 | €20 - 40 |

| 12 years | €6 – 12 | €24 - 48 |

| 16 years | €8 – 16 | €32 - 64 |

Infographic only available in French

Many parents give less than this recommendation, often due to family budget constraints or money received for birthdays and holidays such as Christmas. It is therefore important to take these factors into account to find a balance between learning and family circumstances.

Cash or electronic money

Most parents give pocket money electronically. However, for younger children, cash is preferable as it is more concrete and tangible for them.

- From secondary school onwards, it can be useful to open a bank account for your child:

- The child can learn budgeting by checking their balance and seeing the immediate impact of each expense.

- They learn to use a debit card and a banking app, and to make transfers.

- They learn to make online purchases safely, an essential skill in the digital age.

- The child or teenager can develop independence in a supervised way thanks to age-appropriate limits and settings, while parents can retain control via their banking app.

Payment frequency

Most parents (50.4%) give pocket money monthly, while 37.4% do so weekly.

Liesje recommends giving pocket money weekly to younger children, as a month is too long for a seven-year-old. If not all of the money is spent, she suggests moving to a fortnightly system.

By contrast, a 12-year-old is generally able to manage a monthly budget, although some may require a shorter period.

Common challenges and practical solutions

Parents often find it difficult to manage their children’s pocket money. Here are the most common situations and expert advice.

Balancing spending and saving

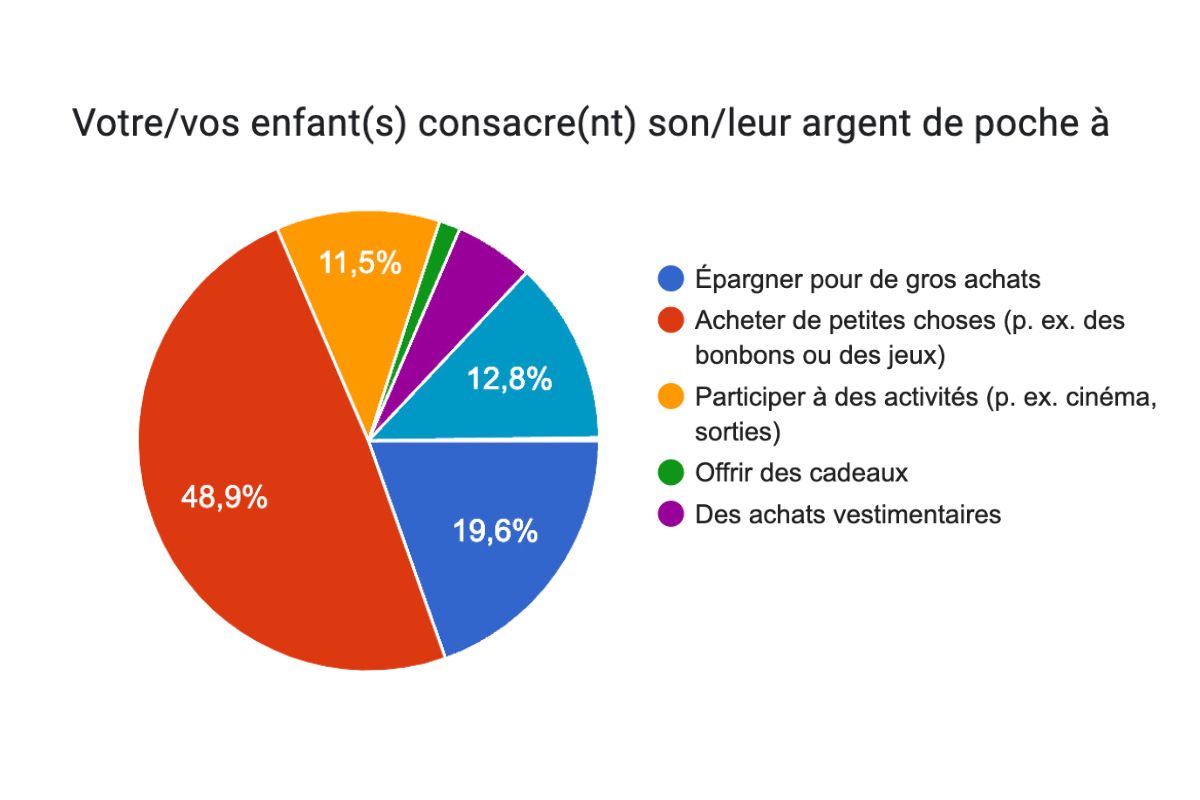

The survey reveals that children primarily use their pocket money to purchase small items (48.9%), such as sweets or ice cream. A smaller proportion is saved (19.6%), although most parents (52.2%) would like their children to save more.

Parents can encourage saving by helping children create a simple budget, dividing pocket money between immediate spending, savings and future purchases. Talking about financial choices helps children to understand the value of money and to distinguish between needs and wants.

If a child or teenager spends all their money at the start of the month, this can be a valuable learning experience. They are more likely to manage better next time. Mistakes are part of learning.

Resist the temptation to give repeated advances. Experiencing a temporary shortage is a more effective way of learning to budget than any lecture.

“When pocket money is limited, it's important to discuss this with your child. What values do you want to pass on? For example, you could discuss avoiding spending on products that promote violence, sweets or slime. Learning to spend means understanding value and managing a budget.”

Liesje Vanneste, financial education expert

Infographic only available in French

Extra money and small jobs

Children can sometimes take on small jobs to earn more money. Just over half of parents say that their child under the age of 15 do odd jobs for neighbours or sell second-hand items to earn extra money.

According to Liesje, these initiatives are beneficial. They help young people understand that earning money requires time and effort, and that work has value. However, she highlights a legal grey area, as students are only permitted to work from the age of 15 in Belgium.

She also emphasises that pocket money should not be a reward for doing household chores, but rather a regular allowance to help children learn to budget.

'You obviously should not give your child money for emptying the dishwasher. They are part of a family, and certain tasks must be done. You don't get paid for that.”

Liesje Vanneste, financial education expert

Among the parents surveyed, 17.4% reward their children for household tasks, typically for larger chores rather than daily ones.

Banking solutions to support learning

Opening a bank account for children or teenagers helps them understand money management and digital banking. It also allows them to learn long-term financial habits, including saving and interest via a linked savings account.

To offer your child their first banking experience, BNP Paribas Fortis offers the Welcome Pack, a free youth current account for children and teenagers up to age 18. This account allows your child to manage their money independently, while you retain parental control.

With Easy Banking App and the online Easy Banking Web, children can check their balance, track spending and carry out simple transactions securely via smartphone or computer. The payment card helps them learn essential banking habits.