Should we be concerned about a private credit crisis in the United States?

5 min

U.S. private credit is unsettling the markets. Are investors about to relive the 2008 crisis?

Private credit raises concerns

- The debate around U.S. private credit has intensified in recent weeks, causing some unease in the markets.

- Some observers are concerned about the concentration of private credit in certain sectors and the systemic risks this could create.

- Others believe that the sector’s growth has been excessive.

- Is the current situation comparable to the period leading up to the 2008 crisis?

The starting point for this discussion lies in the financing of mid-sized companies. These businesses generally do not have access to public markets (bonds or equities) and must therefore turn to private credit, which is dominated by a handful of major players such as Blackstone, Apollo Global Management and Ares Management.

In the United States, the private credit sector expanded significantly after 2008, when a wave of bank failures led regulators to tighten the lending framework for banks. Yet the companies that rely on this type of financing play a crucial role in the U.S. economy, accounting for almost 50 million jobs and around one-third of GDP.

What is driving concerns about U.S. private credit?

The unease emerged in the first quarter of this year, when investors sought to withdraw more than $10 billion from some of the largest private credit funds. This led investment managers to limit withdrawals, while others, such as JPMorgan, announced higher provisions for future losses on these products.

Some prominent voices on Wall Street have suggested that these tensions resemble the early stages of the 2008 financial crisis. However, others remain sceptical, arguing that these broad sell-offs do not reflect the underlying performance of their portfolios.

SaaS under pressure

Some of the recent concerns have focused on the rapid growth in lending to software services companies, known as SaaS (Software as a Service), as well as other businesses with limited physical infrastructure.

In reality, the typical private credit borrower is a mid-sized company: too large for a small bank loan, yet too small to issue its own bonds. Such companies usually generate between $20 million and $500 million in revenue and tend to borrow from specialised funds rather than from banks.

Banks remain essential for deposits, payment infrastructure and shorter-term lending. However, post-2008 regulations have reduced their risk appetite for lending to mid-sized companies. Private credit has helped fill this gap, although the economy requires both sources of financing to function effectively.

Is the concern about private credit justified?

Before reacting to its rise, it is worth noting that private credit’s risk profile is more conservative than many fear and that it now represents 75% of non-bank financing in the U.S. Leverage ratios (debt relative to equity) are around two times lower than those of large banks.

The funds providing this financing do not rely on federal deposit insurance, meaning that any losses would largely be absorbed by sophisticated institutional investors who understand long-term risk profiles. Unlike in 2008, taxpayers would not be exposed to these losses.

Furthermore, a large share of private credit is structured through closed-end funds and is not funded by bank deposits. In other words, the risk of a traditional “bank run”, where clients suddenly withdraw funds en masse, remains limited.

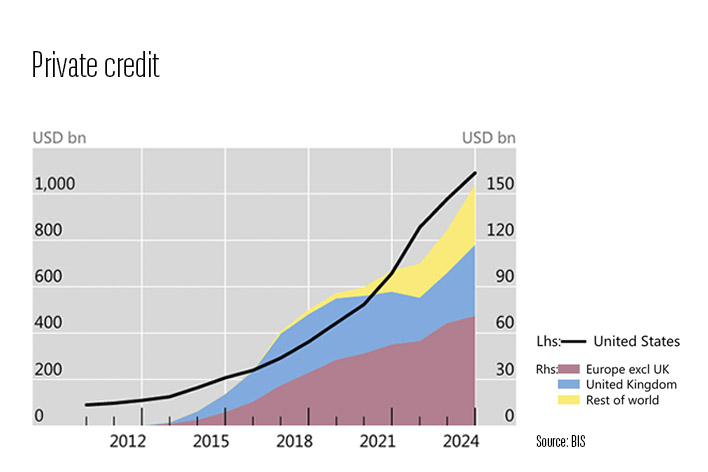

What is the real weight of private credit in the United States?

Despite its strong growth, private credit should be considered in relation to the wider credit system. In the United States, for example, total credit amounts to $104 trillion, $60 trillion of which is extended to the private sector (i.e. households, businesses and banks).

The outstanding private credit that is currently raising concerns amounts to $1.7 trillion, or just 2.8% of total private sector credit.

Should investors fear a shock similar to 2008?

Private credit has developed precisely at times when access to other forms of financing has tightened, for example, during the contraction in bank lending after the 2008 financial crisis or during the Covid pandemic. If investors start selling in the event of a sudden macroeconomic shock, the prices of listed equities or debt can fall rapidly.

However, many private credit funds are long-term and not publicly traded, which helps shield companies and portfolios from market volatility. The financial system’s resilience has never come from uniformity, but from maintaining diverse capital sources that can serve different borrowers under different conditions. In this sense, private credit plays a key role in financing the companies that will create jobs, modernise production and expand into new markets. In short, these are the companies that will drive tomorrow’s economic growth.