First nowcast Q2: growth in times of fiscal restraint

5 min

With only a few weeks' worth of data available, the models show much greater uncertainty than usual. This is further exacerbated by the current highly volatile geopolitical context. Nevertheless, we can already see growth slowing and inflation rising. This is the worst possible scenario for a government seeking to reassure critical rating agencies. This is all the more problematic given that neighbouring European countries are increasing fiscal spending and growing faster than we are.

Energy prices

Despite repeated attempts at negotiations, the situation in the Middle East remains highly volatile. This is reflected in energy prices. Our baseline scenario assumes that prices will not start to fall again until the second half of the year. However, our colleagues at BNP Paribas Group estimate that oil prices will still remain above $80 per barrel next year, more than $10 higher than in our pre-war forecasts.

The impact on inflation is therefore unavoidable. In addition to the direct effect of higher prices, we are also seeing second-round effects that could accelerate food inflation in particular. These effects are most evident in energy-intensive sectors.

Significant price increases are expected in both the construction and industrial sectors, as shown by the latest business surveys. In industry, the share of companies expecting such an increase now stands at 40%. The figure is also 40% in construction. However, this remains below the peak observed at the end of 2021, when as many as 60% of companies expected an increase.

Overall, we expect inflation to be 3.2% this year and 2.0% next year.

Growth ...

In our baseline scenario, GDP is currently expected to grow by just 0.7% this year and 1.1% next year. This is significantly lower than anticipated at the start of the year.

Risks are becoming more balanced. While a prolonged and/or intensified conflict in the Middle East weighs on the outlook, European investment in defence and/or artificial intelligence could, at the same time, accelerate growth.

Our latest nowcast already points in that direction. For the second quarter of this year, based on only a few weeks’ worth of (transaction) data, we estimate growth at 0.1%. This clearly confirms the slowdown we had suspected for several weeks, following a further decline in consumer confidence and rather subdued business sentiment in the latest surveys by the National Bank of Belgium.

Retailers in particular are pessimistic. Confidence in this sector is at a very low level, raising concerns about a slowdown in private consumption, which accounts for nearly half of Belgian GDP.

... in times of spending cuts

The Federal Planning Bureau expects the indexation threshold to be exceeded in July this year. However, given the current indexation mechanism, adjustments to benefits and wages are likely to be more limited than in 2022, for example.

This makes the comparison with the post-Covid energy crisis particularly striking. While governments readily increased fiscal spending at that time, today budgets are firmly constrained.

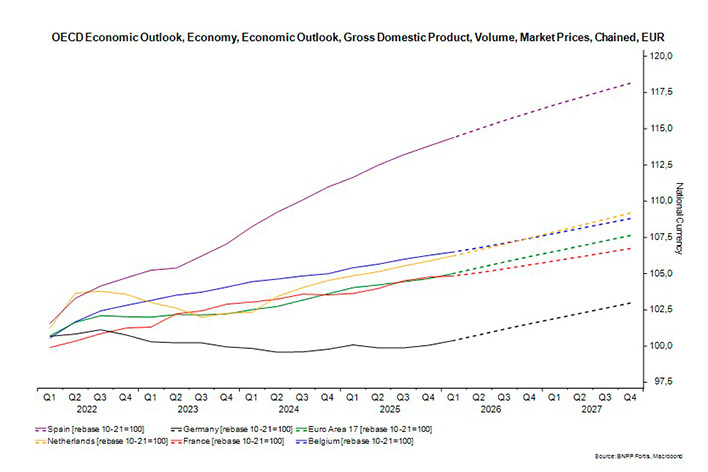

This will weigh on our growth. In the 4 years following the pandemic, the Belgian economy grew by a total of 5% in real terms. This outperformed all neighbouring countries as well as the European average. Germany, in particular, lagged well behind.

However, this is set to change in the coming period, according to OECD forecasts. The Netherlands is making up the ground lost since 2022, while other euro area countries are also, on average, catching up with Belgium. Germany, in particular, is regaining momentum thanks to increased defence spending driving stronger growth.

A low debt ratio combined with additional public spending to support growth is something our government can only dream of today.