Europe, energy and a major misconception

5 min

Europe is economically the richest region in the world, alongside the United States. Yet the continent is structurally weak in one crucial area: energy. It has very limited domestic fossil fuel reserves, imports almost everything and is therefore highly sensitive to any disruption to the global market. This is not a temporary issue. It is a long-standing structural vulnerability.

The figures are sobering. Europe imports 94.8% of its oil. Until recently, its dependence on gas was almost as high: prior to Russia’s invasion of Ukraine, approximately 40% of Europe’s gas supply originated from Russia. When Moscow turned off the gas tap, Europe had to find alternatives at record speed — and at significant cost. It paid premium prices for liquefied natural gas (LNG) from the United States and Qatar, which poorer countries could not compete with.

It used to be different

In the 1980s and 1990s, Europe produced 20–30% of the oil it consumed through Norway and the United Kingdom. The Netherlands was once home to the world's ninth largest gas field. At its peak in 1976, the country produced 90 billion cubic metres of gas, representing 3.3% of the global total of 2,740 billion cubic metres. By 2011, production had fallen to around 80 billion cubic metres, accounting for just 2% of the global total.

This domestic buffer has now almost entirely disappeared, while import dependency has continued to grow. Consequently, Europe has become a classic 'price taker': while it carries economic weight as a major consumer, it has little or no control over supply sources.

Gas is the weakest link

In times of crisis, oil dominates the headlines. However, for Europe, gas is actually the most important commodity. Gas drives electricity prices. The price of electricity is determined by the most expensive energy source needed to meet 100% of demand. When renewable energy and nuclear power are insufficient, gas-fired power stations are brought into operation. Gas is also needed to heat millions of households and is essential for a wide range of industrial processes. Therefore, a disruption in gas supply affects Europe on multiple fronts at once.

A new energy crisis?

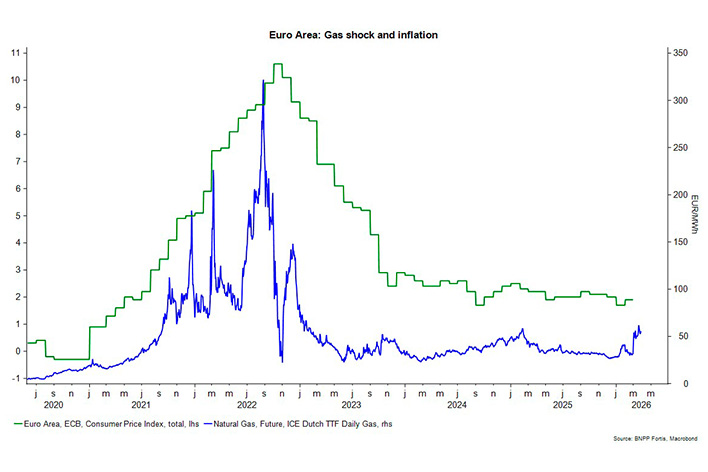

The recent closure of the Strait of Hormuz illustrates this clearly. Although the media tends to focus on oil, it is the price of gas that is having the greatest impact on the European energy market. Gas prices have risen significantly, inevitably drawing comparisons with the energy crisis of 2022.

However, the market is interpreting this shock differently this time around. In 2022, the loss of Russian gas was considered permanent and structural, supplies were not expected to resume. The current disruption, although serious, is still considered to be only temporary. This difference in perception is reflected in prices: despite recent increases, they remain well below the 2022 peak.

There is also a macroeconomic difference. In 2022, inflation in Europe was already very high due to the impact of the pandemic. Lockdowns triggered a sharp increase in the price of goods, as strong household demand was met with a shrinking supply due to disrupted supply chains. When economies reopened, demand for services surged, creating a second demand shock. This sequence of shocks took central banks by surprise, and their gradual interest rate increases failed to keep pace with events. The result was persistent, broad-based price rises.

Today, however, the situation is different: inflation is close to the European Central Bank’s target, and European labour markets have weakened considerably. This time, the supply shock is not accompanied by a demand shock. This reduces the risk that a one-off energy price increase – the duration of which remains uncertain — will lead to sustained inflationary pressure.

A different dependency

This is no reason to become complacent. Following Russia’s invasion, Europe built 25 new LNG terminals. This additional capacity corresponds to 41% of the EU's total gas demand, and exceeds previous Russian imports. However, these terminals do not solve the fundamental problem. They make Europe more dependent on LNG imports by sea, making it vulnerable to new disruptions, as demonstrated by the closure of the Strait of Hormuz. It is a change in dependency, not a reduction.

The misconception about renewable energy

A dangerous misconception clouds public debate in this area. Today, 47% of Europe’s electricity comes from renewable sources, such as wind, solar and hydropower. This is an impressive achievement. However, anyone who believes this means we are halfway towards a fossil-free economy is making a fundamental calculation error.

Electricity accounts for only 20–25% of total energy consumption. The remaining 75–80% is used for transport, industry, and heating — sectors in which oil and gas still dominate. In fact, when you work through the numbers, you find that renewable energy accounts for only 10 to 12% of total European energy consumption. Oil alone still represents 30–35% of total global energy consumption — three times more than renewables.

Take the transport sector, for example. In Europe, 66% of all oil products are used for transport and 91% of the sector's final energy consumption still comes from fossil fuels. While the share of electric passenger cars is growing rapidly, trucks, aircraft and container ships still largely run on oil and kerosene. Although newer aircraft consume up to 30% less kerosene than before, this is an efficiency gain rather than a replacement.

The infrastructure of the European economy, including ports, refineries, heating systems and industrial installations, is built around fossil fuels. Transforming this will take decades, not years. As long as this reality is not fully acknowledged, policy expectations will remain too high and energy policy will remain fragmented.

The real challenge

The combination of structural import dependency, the central role of gas in the European economy and the limited scope of the current energy transition makes Europe a particularly vulnerable continent. It is not hopeless, but it is vulnerable. The solution is to reduce dependency, not to replace it with a different kind of dependency. This requires accelerated investment in renewable energy, energy efficiency, and an integrated European electricity network.

However, it also requires honesty. As long as transport, industry and heating continue to rely heavily on fossil fuels, every crisis in an oil- or gas-producing region will remain a European crisis. We are decarbonising quickly in the easiest areas. The more difficult sectors are yet to follow suit.